Residential lending standards have come a LONG way since the 2008 GREAT recession. It is much harder to qualify for a mortgage today than it was before the 2008 recession. Today 95% + of loans qualify show income in the form of tax returns, w-2, retirement income, and reported self-employed income. There are alternatives to this, 12/24-month bank statements or maybe a DSCR loan on investment property but those loans make up such a small percentage of the overall loans. Prior to 2008, the JOKE was “all you needed was a heartbeat and pen” to get a loan and unfortunately it was that easy to get a loan.

Today the average credit score, profile of the borrower, ability to repay, type of loan products and down payments are a BIG difference. The days of the options ARMS, teaser ARMS, and basically the loans set to make a borrower fail have gone away.

85% of Americans have an interest rate of 5% or less and out of those mortgages, about 95% of those are fixed-rate mortgages. Over 50% of those fixed-rate mortgages are under 3%. Borrowers took advantage of the low rates and locked in low fixed payments and are sitting in a really good position.

Do you think this is helping the housing market avoid another CRASH?

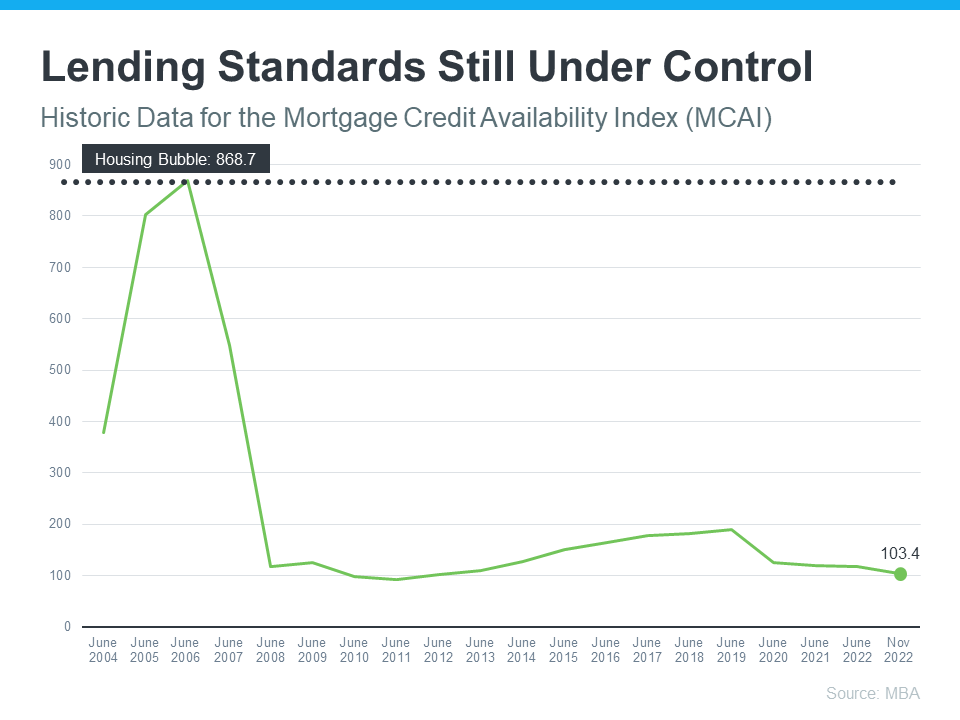

Below I provided charts to show that lending standards are about 80% better.

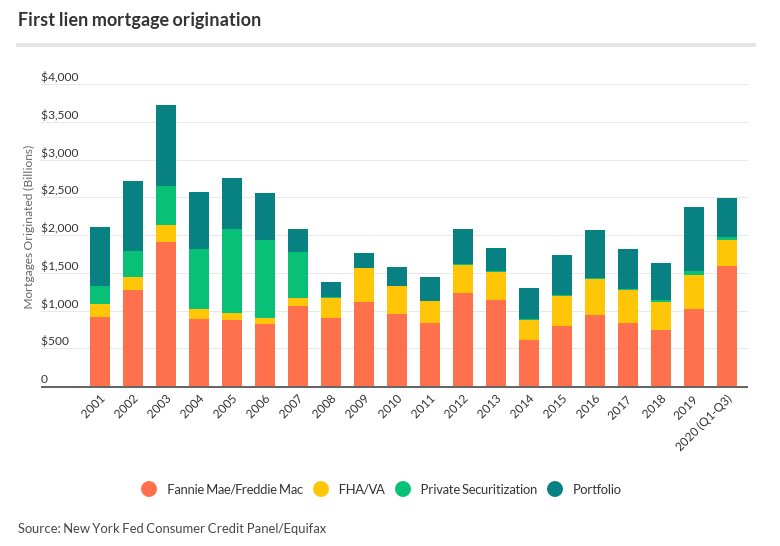

What I wanted to point out in the chart below were the private securitization loans. Did you notice how they are such a small % today compared to back before 2008? Those are the loans that are created and sold on the secondary market, think of NON-QM loans today and before 2008 well those were ALL the loans that were very easy to get and had a BIG impact on hurting the housing market when the market had a correction.

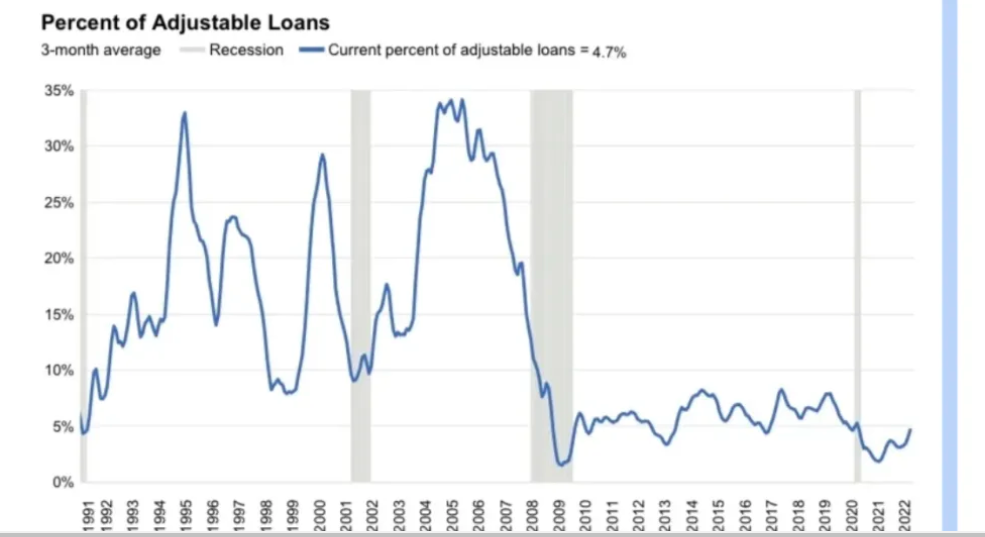

The chart below shows a massive drop in ARM loans after 2008.

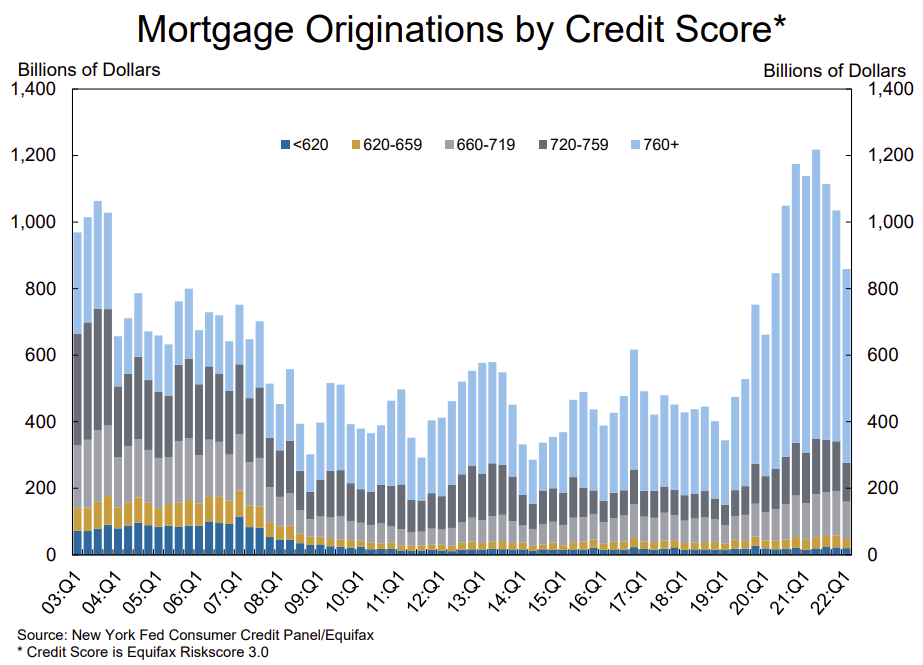

The chart below you can see the average credit score go UP since 2008 for mortgages.