Fannie and Freddie are at it again. F&F is going to start hitting you harder for cash-out refinances, investment properties, high credit, more down, Higher credit scores, DTI over 40%, and the list goes on. F&F say they are taking the extra revue from the higher borrowers to give to the borrowers that have lower credit, less down, and need more help. Not sure if anyone agrees with this and if this will hold up long-term. NAR already sent a letter to F&F about the 40% DTI hit asking them to reconsider it since rates are already high in today’s real estate market.

What do you mean by “fees/costs?” This refers to Loan Level Price Adjustments (LLPAs) imposed by Fannie Mae and Freddie Mac (the “agencies”), the two entities that guarantee a vast majority of new mortgages. LLPAs are based on loan features such as your credit score, the loan-to-value ratio, occupancy (owner vs non-owner occupied homes), and most recently, your debt-to-income ratio

What lenders/loans does this apply to? Any loan is guaranteed by one of the agencies regardless of the lender. These are MOST loans in the US. Examples of loans that wouldn’t be affected would be FHA/VA as well as certain jumbo and specialty products. “Non-conforming” loans are not impacted by this as they are not guaranteed by the agencies. A common example of a non-conforming loan would be a jumbo loan from a retail bank or credit union.

When does this take effect? This applies to loans that are guaranteed by the agencies starting May 1st, 2023. That means many lenders will begin implementing the changes in March/April.

Imagine this scenario:

LO: Hello Borrower, sorry but your interest rate is higher now because your DTI is over 40%.

Borrower: Hmm, I wouldn’t say I like the sound of that. What if I put more down and go from 95 LTV to 85 LTV?

LO: Well Borrower, if you do that your rate will get worse.

Borrower: If I put more down, my rate gets worse. So first you tell me my rate is X, now you tell me my rate is X+ 25% due to DTI even though I gave you all my income docs before you disclosed and now, you’re saying if I put 15% more down, my rate goes to X+0.375%? I am going to call the CFPB since this clearly can’t be accurate.

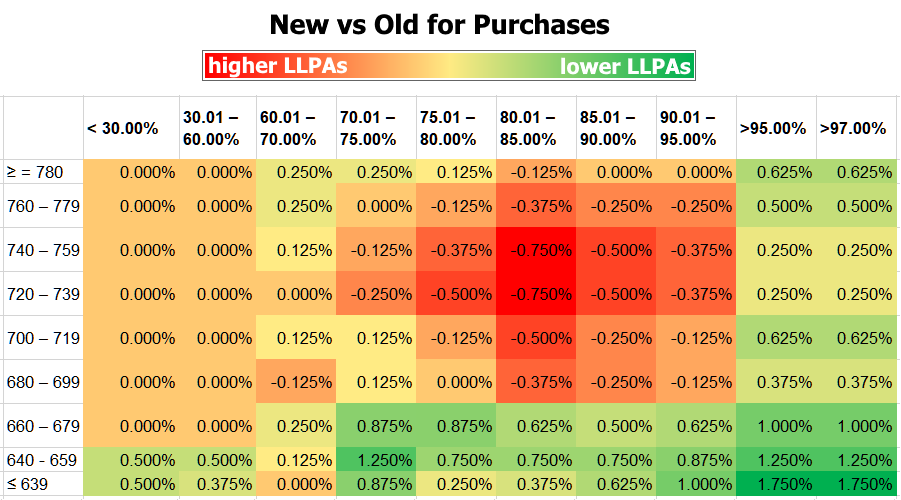

If you look at the chart, you can see that if you have a 720 credit score and put down 20% it is a .5% hit to the cost of a loan, but if you have a 639 credit score it is only a .25% hit to the cost of the rate.

If you have any questions, please reach out to us 😊