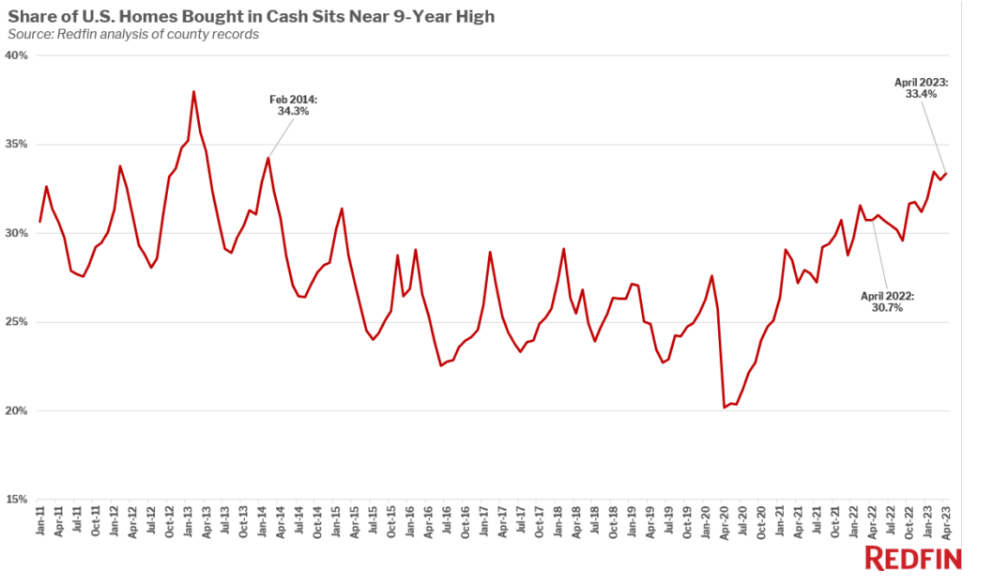

According to a recent Redfin study, April 2023 saw the highest share of all-cash home buyers in the last nine years. Nationwide, 33% of transactions closed were all-cash, with some markets seeing even higher rates. For example, some markets in Florida, Ohio, Maryland, and New York show 50% more all-cash buyers.

Some factors could be contributing to this trend, including low-interest rates, rising home prices, and a shortage of inventory. Low-interest rates make it more affordable for buyers to pay cash for a home while rising home prices make it more difficult for buyers to qualify for a mortgage. The inventory shortage means fewer homes for sale, which gives all-cash buyers an advantage.

The increase in all-cash buyers could have several implications for the housing market. It could lead to higher prices, as all-cash buyers are often willing to pay more than buyers who are financing their purchase. It could also make it more difficult for first-time homebuyers to compete in the market.

It is important to note that the data from Redfin is based on closed transactions. The share of all-cash buyers may be even higher in some markets, as some buyers may choose to pay cash even if they can qualify for a mortgage

High mortgage rates, cash on hand, and selling a property with lots of equity are the BIG drivers of why someone would pay cash. If you have the opportunity, then why not? You can always refinance later when rates drop if it makes sense. Lots of buyers are trying to be competitive so if you can write an ALL cash offer, with no contingencies and a 7-day closing that is very appetizing for a seller in today’s low inventory environment.

Let’s be honest, who has this kind of cash sitting around? 1% of buyers? The answer is NOT really, there’s lots of money on the sidelines for so many reasons. Baby Boomers make up the largest share of those buyers, ages 58 to 76. They make up more than 50% of the cash buyers in today’s market. Think about it, it is the younger buyers that want to take out a loan to purchase a property, when you are getting older you do NOT want debt. 40% of the homes in the US are free and clear, which is a crazy number to think about. Out of the 60% that is left, 92% have a rate of SUB 5%, 75% have a rate of SUB 4% and about 26% have a rate of 3% or less. So, the mortgage properties are sitting on a very nice 30-year fixed low rate, low payment, and owners are feeling great about this

There are markets in NY, FL, CA, and more where there is the 1% that can pay cash anytime and that are buying these high-end properties. Cash buyers are NOT a new thing, this trend comes and goes as you can see in the chart above. Being a cash buyer can really set you apart and help to get your offer accepted. There are also flippers, I buyers, wall street firms, and investors that make up a BIG portion of the cash buyers as well. They might be looking for more of a deal or a dilapidated property where there is upside, most of the time they are cash buyers or a quick close with private money that is almost the same thing.

I talk to people daily that are house trapped by a low mortgage rate which really means a low mortgage payment. So many people have looked at what it would mean to sell or even keep their home to buy a new one. When they look at the prices, rates, terms, and what we all really care about monthly payment it makes ZERO sense to do anything. So, if more people had cash lying around, they would buy and just keep what they had or they could sell and pay cash. That is hard because most of the people I am talking to want to buy up or buy in a different location. Most don’t have the option to do this so they will stay for now.

I guess time will tell how long and what will ultimately bring us more inventory. Maybe the real estate ice age is real, and most sellers are frozen or stuck where they are simply because they have the lowest payment they will ever have. There are lots of articles or posts talking about how rates will never get back down to the 2’s, 3’s and people say even the 4’s. Maybe they are right but maybe they are wrong. If the 10-year treasury drops to 2.5% and the spreads move to more of a normal 1.6 to 1.8% over the 10 YR T, that puts rates into the around 4.375% for a conventional 30-year fixed. FHA/VA rates are typically .5% lower, so that puts us around 3.875% and ARM rates are typically .5% lower, so they could be in the high 3’s as well.

Cash is KING and always will be because you are not deciding to buy something based on the rate/payment. You are buying because you can and that is a great position to be in.